NewRez is closely monitoring the evolving situation of COVID-19 and is providing an update on temporary guidance while we navigate through this uncertain time. This announcement provides flexibilities for conventional conforming loans due to the disruption of business operations or the inability for an appraiser to perform an interior inspection per Fannie Mae Lender Letters LL-2020-03 and LL-2020-04 and Freddie Mac Bulletin 2020-5. Note that these flexibilities do not extend to conventional conforming loans originated in conformance with state Bond or HFA programs.

These temporary flexibilities are effective immediately for all conventional conforming loans in process and remain in place for loans with applications dated on or before May 17, 2020.

We will continue to provide updates as the situation changes.

fannie mae and freddie mac products only

Employment Verification

Verbal Verifications of Employment

Every attempt should be made to obtain a verbal verification of employment (VVOE) confirming the borrower’s employment within 10 days of the Note date. If this is not possible, then a paystub may be obtained. Note – a reasonable attempt should be made for each option, including the verbal verification. At least 24 hours should be given for each applicable attempt.

- Email Directly from Employer: An email may be used to verify the borrower’s

employment within 10 days of the Note date. When email is used, it must:- Be from the employer’s email address, such as name@company.com (no Gmail, yahoo, etc.)

- Be from the borrower’s direct supervisor/manager or the employer’s Human

Resources department, - Contain all the standard information required on a VVOE, including the name, title, and phone

number of the person providing the verification, and - Identify the borrower’s name and current employment status.

- Paystub: A year-to-date paystub from the pay period that immediately precedes the Note date.

The income should be consistent with the paystub used for qualification and the AUS findings, with no decrease or adverse change in earnings. - Self-Employed Borrowers

Verification that the borrower’s business remains operational must be done within 10 days of the Note date.

NewRez will not accept bank statements as alternative documentation to the VVOE.

DU Validation Service and LPA AIM

If employment has been validated by DU validation service or LPA AIM, that validation will remain eligible as long as the “close by” date is complied with. Otherwise, follow above guidance.

Continuity of Income

Due diligence must be practiced ensuring continuity of income while determining that the most recent employment and income information is obtained. It is critical that the borrower’s ability to repay the mortgage is not negatively impacted.

- Borrowers who have been temporarily laid off, furloughed or are otherwise not receiving the income disclosed for purposes of loan qualification are not eligible unless:

- additional, acceptable, qualifying income is verified and adequately supports the borrower’s ability to repay, and

- the income meets the requirements of Fannie Mae or Freddie Mac Selling Guides

Property Valuations - Appraisal Flexibilities

See Announcement 2020-048 dated April 17, 2020 for updated guidance.

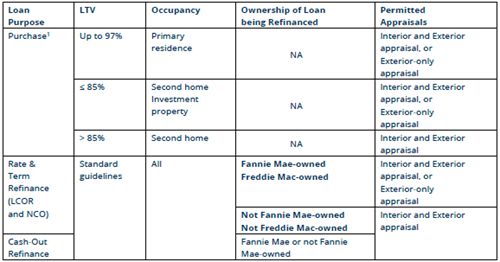

Effective immediately, NewRez will allow temporary flexibilities to appraisal inspection and reporting requirements with the exclusion of Texas 50(a)(6) loans. When an interior inspection of the subject property is not feasible due to COVID-19 concerns by either the appraiser or borrower, an exterior-only inspection appraisal will be permitted based on the following:

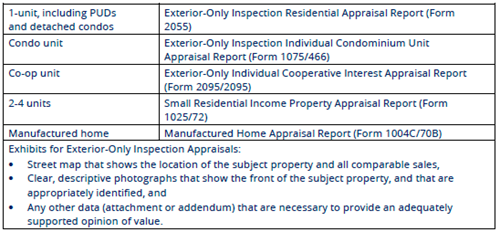

Exterior-Only Inspection Appraisals

An exterior-only inspection appraisal may be obtained in lieu of an interior and exterior inspection appraisal for the following:

- Purchase transactions

- Rate & Term refinance transactions where the loan being refinanced is owned by Fannie Mae or Freddie Mac

Conventional conforming loans with an existing appraisal order will be evaluated for conversion to an Exterior-Only Inspection in accordance with the above guidance. You will not need to reach out to the applicable AMC.

Identification of a Fannie Mae or Freddie Mac Loan

Use the following loan lookup tools to determine if Fannie Mae or Freddie Mac are the current investor of the existing mortgage.

• Fannie Mae Loan Lookup tool

• Freddie Mac Loan Look-Up tool

Revisions to Scope of Work, Statement of Assumptions and Limited Conditions, and Appraiser’s Certification

The following documents include modified language to be used with a desktop appraisal or exterior-only appraisal reports:

- Modified Set of Instructions, Scope of Work, Statement of Assumptions and Limiting Conditions and Certification for Desktop Appraisals

- Modified Set of Instructions, Score of Work, Statement of Assumptions and Limited Conditions and Certification for Appraisals with Exterior-only Inspection

These documents include modified language for the scope of work, statement of assumptions and limiting conditions, and certifications. It is important to note that certification #10 has been removed in recognition that the appraiser may have relied on information from an interested party to the transaction (borrower, realtor, property contact, etc.) and additional verification may not have been feasible. Appraisal reports submitted using the flexibilities provided in this Announcement must include these documents with the modified language for scope of work, statement of assumptions and limiting conditions, and certifications.

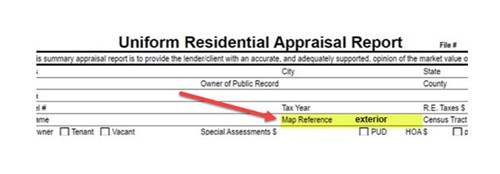

Additional Instructions for Appraisals

For an appraisal with an exterior-only inspection that is completed on a form for an interior and exterior inspection (e.g., Form 1004/70), as permitted above, the appraisal report must include, in the “Map Reference” field, the corresponding text identifier that verifies the type of appraisal completed; specifically, “exterior.”

Completion Reports

Properties appraised completed “subject to” require an Appraisal Update and/or Completion Report (Form 1004D/442). If no completion report is available due to COVID-19 related issues, a signed letter from the borrower confirming that the property was completed with any of the following evidencing completion will be permitted:

- Photographs,

- Paid invoices indicating completion,

- Occupancy permits, or

- Other substantially similar documentation

Appraisal Waivers

It is recommended that the borrower accept an appraisal waiver offer provided through either Desktop Underwriter or Loan Product Advisor. Remember to submit loans to AUS prior to obtaining an appraisal.

Freddie Mac has announced that they will be expanding ACE waiver through LPA with new submissions on or after March 29, 2020. Their change will align with current Fannie Mae Appraisal Waiver Policy. Fannie Mae and Freddie Mac both continue to evaluate further expansion options, but no additional updates have been provided.

Closing Agent as Power of Attorney (Fannie Mae loans only)

A closing agent or other affiliated party may sign loan documents on the borrower’s behalf using a power of attorney for rate and term refinance transactions subject to the restrictions in Selling Guide B8-5-05 Requirements for Use of a Power of Attorney.

For rate and term refinance transactions, an individual who would otherwise be prohibited from serving as an attorney-in-fact or agent may execute the required loan documents on behalf of the borrower(s), provided all the following conditions are met:

- The attorney-in-fact or agent is not an employee of the lender.

- The power of attorney expressly states an intention to secure a loan not to exceed a stated amount from a named lender on a specific property.

- The power of attorney expressly authorizes the attorney-in-fact or agent to execute the required loan documents on behalf of a borrower only if the borrower has, to the satisfaction of the attorney-in fact or agent in a recorded, interactive session conducted via the Internet, both

• confirmed his or her identity; and

• reaffirmed, after an opportunity to review the required loan documents, his or her agreement to the terms and conditions of the required loan documents evidencing such transaction and to the execution of such required loan by such attorney-in-fact or agent.

For additional information, below are links to Fannie Mae and Freddie Mac Frequently Asked Questions

Remember that NewRez is not adopting all flexibilities in the Fannie Mae and Freddie Mac announcements, therefore some guidelines in their announcements and FAQ may not apply.

Please reference the NewRez Lending Library for the changes outlined in this announcement.